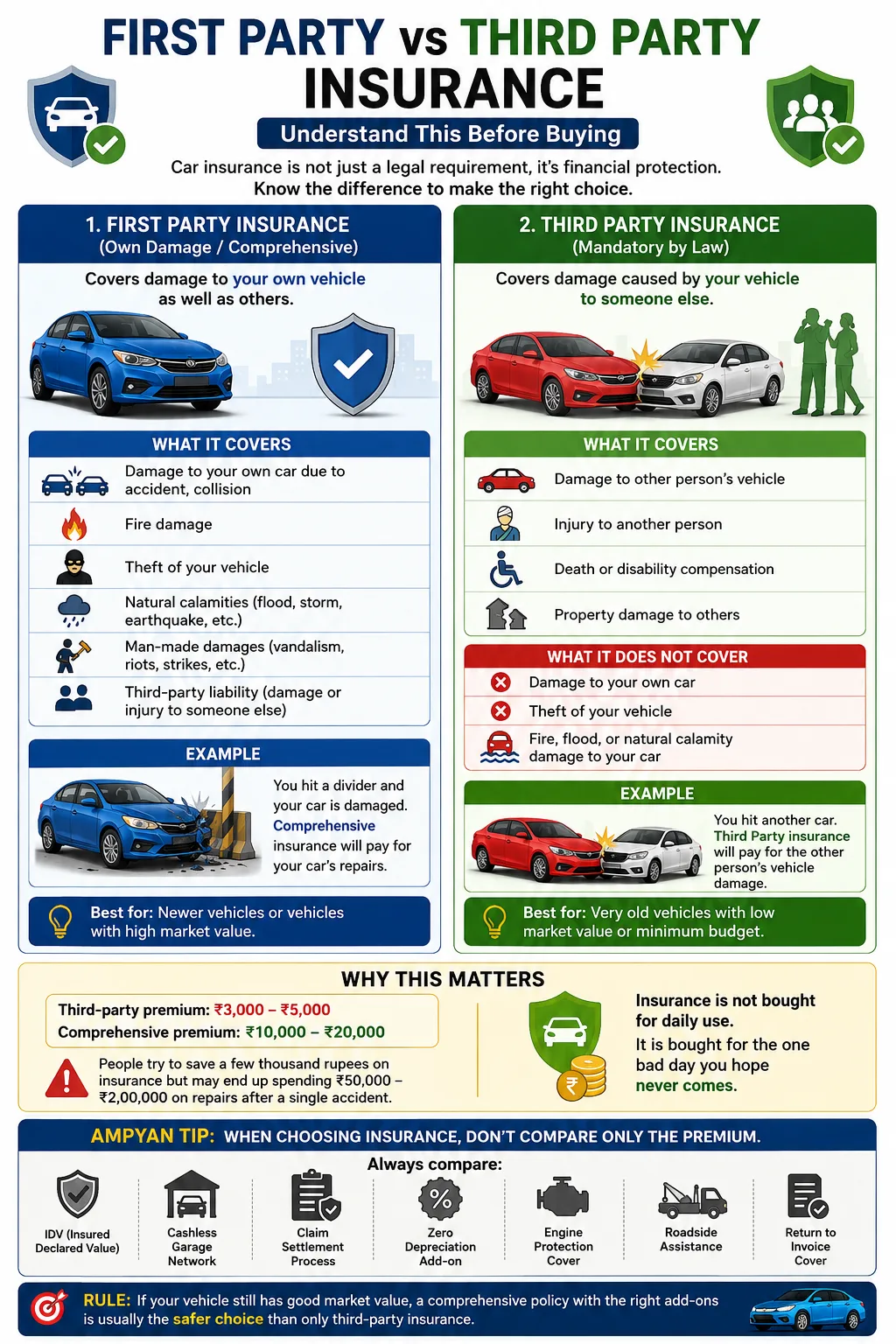

Many vehicle owners buy insurance only because it is mandatory. But understanding First Party and Third Party insurance can save you from huge financial losses later.

1. Third Party Insurance (Mandatory by Law)

Third-party insurance covers damage caused by your vehicle to someone else.

Example:

You accidentally hit another car, bike, person, shop, or property.

Insurance pays for:

✅ Other person’s vehicle damage

✅ Injury to another person

✅ Death or disability compensation

✅ Property damage to others

Insurance does NOT pay for:

❌ Damage to your own car

❌ Theft of your vehicle

❌ Flood, fire, accident damage to your car

Who should consider it?

* Very old vehicles with low market value

* Owners willing to bear their own repair costs

Reality Check

Many people buy third-party insurance because it is cheap. But one major accident can result in repair bills worth lakhs for their own vehicle.

⸻

2. First Party Insurance (Own Damage / Comprehensive)

This covers your own vehicle.

A comprehensive policy generally includes:

✅ Third-party cover

✅ Accident damage to your car

✅ Fire damage

✅ Flood damage

✅ Theft protection

✅ Natural calamities

✅ Man-made damages

Example:

Your car hits a divider.

Third Party:

❌ Your repair bill is yours.

Comprehensive:

✅ Insurance pays as per policy terms.

⸻

Why This Matters

Imagine:

* Third-party premium: ₹3,000–₹5,000

* Comprehensive premium: ₹10,000–₹20,000

People often try to save ₹10,000 on insurance but later spend ₹50,000–₹2 lakh on repairs after a single accident.

Insurance is not bought for daily use. It is bought for the one bad day you hope never comes.

⸻

AMPYAN Tip

When choosing insurance, don’t compare only the premium.

Always compare:

* IDV (Insured Declared Value)

* Cashless garage network

* Claim settlement process

* Zero depreciation add-on

* Engine protection cover

* Roadside assistance

* Return to invoice cover

A cheap policy is only useful if it actually helps when you need it most.

Rule: If your vehicle still has good market value, a comprehensive policy with the right add-ons is usually the safer choice than only third-party insurance.